Could traditional pensions make a comeback in the private sector?

IBM's move could be the harbinger of a trend

Did IBM just kick off the next big trend in the world of employee retirement benefits?

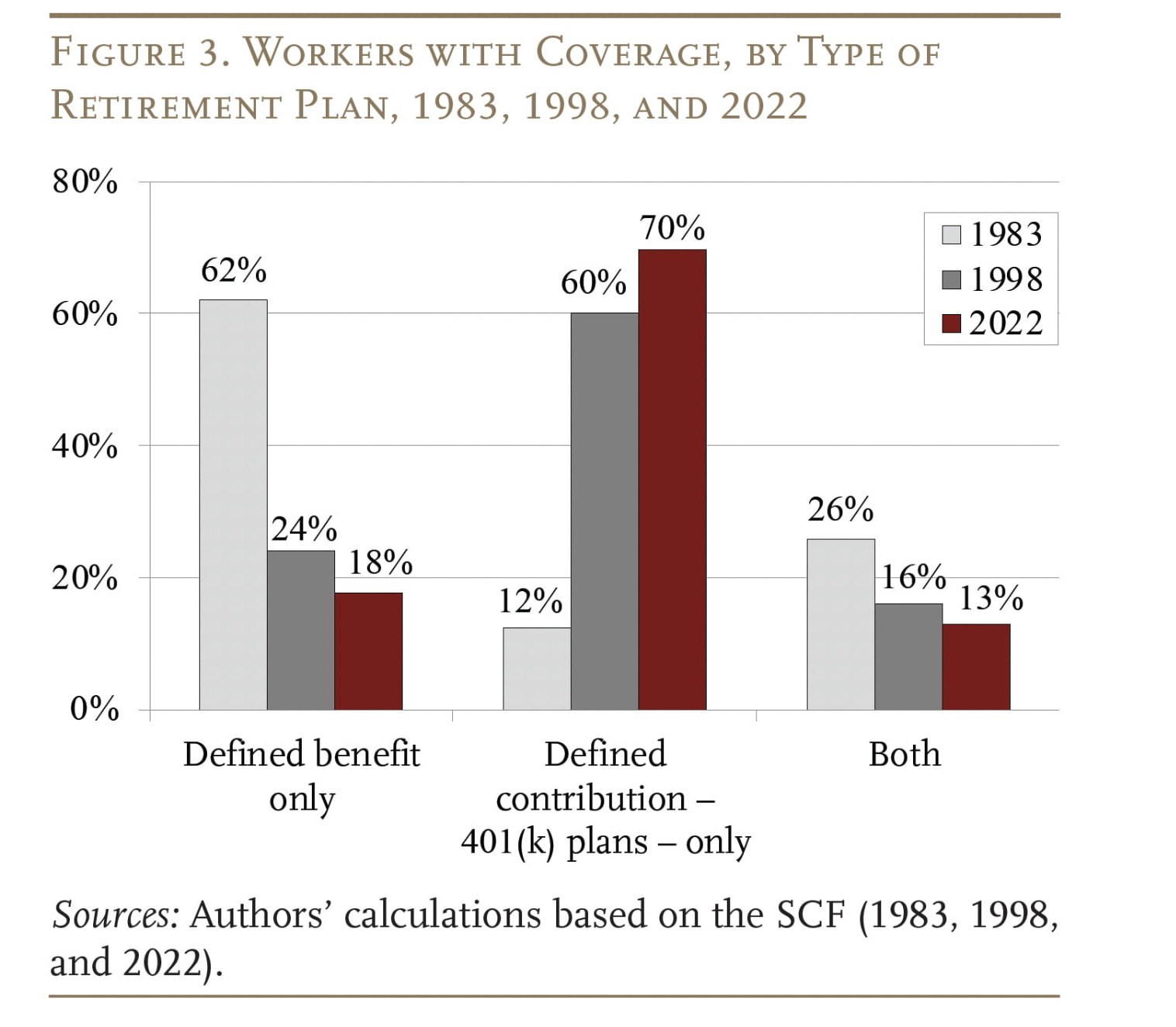

Big Blue made headlines recently when it announced plans to end its 401(k) matching contribution in favor of a new benefit that sure sounds alot like a good old-fashioned pension. While pensions are still dominant among public-sector state and municipal employers, they have all but disappeared in the private sector as employers rushed to get them off their balance sheets over the past two decades.

That much is clear in this chart from the Center for Retirement Research at Boston College (CRR), which depicts data from the Federal Reserve Survey of Consumer Finance:

IBM, often viewed as a leader in the corporate world, was one of the first large employers to announce a shift to an all-defined contribution retirement program in 2006, and the decision was a harbinger of a plunge in the number of employers offering traditional pensions.

Now, IBM will introduce a Retirement Benefit Account (RBA) for all of its U.S. employees. Employees can continue to contribute to their 401(k) accounts. But the match will be replaced by a contribution of 5% of pay to the RBA, along with a one-time pay increase of 1%. The pay credits will accumulate interest credits at a rate of 6% for the first three years, and will be tied to Treasury rates in the years that follow, with a floor of 3% for the first seven years.

The RBA is a defined-benefit structure known as a cash balance plan. Employees do not have individual accounts; instead, the plan “defines” a benefit it will pay from its general assets. The benefit is defined as a lump-sum amount that can be paid in retirement as an annuity calculated to equal the lifetime value of your accumulated sum.

You might be thinking you could beat that 6% return in the stock market - and perhaps you could in any given year. But that won’t happen every year - you’re still exposed to market risk, especially if equities tumble near your point of retirement when you need the money (see: sequence of return risk). Meanwhile, that 6% in the RBA is guaranteed. “ I can't go out and find a whole lot of triple A bonds that will pay me 6% these days,” says John Lowell, a partner at October Three, a firm that provides consulting services to plan sponsors.

IBM is not saying much about its motivations. But conversations I’ve had recently with benefit consultants suggest these reasons for the shift:

A universal benefit: All of IBM’s employees will participate in the RBA, and receive the same annual contribution. That is different from the typical defined-contribution plan, where participation is voluntary - and only about 15% of savers have the financial wherewithal to contribute enough to get the full matching contribution., according to Vanguard data. By contrast, any form of universal defined-benefit plan helps combat rising wealth inequality in retirement.

Retirement income streams: The RBA also addresses the problem faced by employees in converting 401(k) balances into steady streams of retirement income. Employers and policymakers have recognized that problem, as evidenced by the U.S. Congress passing the Secure Act of 2019, which cleared the path to add insurance company annuities in defined-contribution plans. But defined-benefit plans offer a much more efficient way to provide a guaranteed income stream.

401(k)s fail to get the job done for many. The median balances held by individuals in 401(k) and IRA accounts (combined) was just $150,000 in 2022, according to the Federal Reserve data and depicted by CRR in the chart below. That’s not nearly enough to carry people through retirement.

Meanwhile, frozen pension plans at companies like IBM are now overfunded, making it easier to restart the plans. That results from the strong performance of equity markets over the past decade and, more recently, higher interest rates.

IBM is not the only employer thinking about restarting a defined-benefit plan. Jonathan Price, who leads the national retirement practice at benefits consulting firm Segal, said he has fielded more calls about unfreezing or starting a new pension plan in the past year than he has in the past decade.

In a research paper published earlier this year, experts at J.P. Morgan Asset Management argued that the table has been set for a revival of defined benefit plans in the private sector. Sponsors, they argued, have developed a “collective blind spot” about defined-benefit plans, based on historical shortcomings that no longer exist. They noted that today’s private-sector plans are well-funded, and that sponsors have learned the lessons from the problems sparked by the bursting of the tech bubble in 2000, when aggregate funding levels plunged.

In my latest Reuters column, I report on IBM’s decision.

Dying broke: NYT series on the crisis in long-term care

The New York Times has been running an excellent series detailing how the immense financial costs of long-term care drain older Americans and their families. The stories are collected on this page, which is accessible to readers with NYT subscriptions or, in some cases, free registered accounts. Here’s a free link to one of the stories that ran this week on the desperate search for affordable home care that many families experience.

ICYMI: Social Security’s customer service keeps getting worse

I reported last week for the Times on the effect that years of budget cutting by Congress has had on the customer service provided by the Social Security Administration.

The problems include long wait times on the agency’s toll-free phone line, a large backlog in disability applications and controversial clawbacks of overpayments to low-income and disabled beneficiaries.

Many of the problems stem from austere administrative budgets imposed by Congress over the past decade. Since 2011, congressional cuts to the agency’s customer service budget total 17 percent after adjustments for inflation, and staffing fell to a 25-year low last year, according to an analysis by the Center on Budget and Policy Priorities, a research and policy organization. At the same time, the number of beneficiaries rose by 22 percent over the past decade.