Delayed Social Security claiming: the message is getting through

The share of Americans claiming retirement benefits at later ages has continued to rise.

Whenever I write about the question of when to claim Social Security benefits, I underscore the idea that there is no one-size-fits-all answer. But for most people, a delayed claim is compelling from a financial standpoint.

You can file for a retirement benefit as early as age 62, but most people will be better off delaying their claim. For every month of delay, up to age 70, your monthly benefit increases to reflect the delay in claiming. That said, there can be very good reasons to claim early—for example, if you are in poor health and do not expect to have great longevity. And delaying your claim could be challenging if you need to fund living expenses while you delay by working longer or drawing down savings. That is not always possible.

The Social Security rules are designed to pay everyone roughly the same lifetime benefit, no matter when they decide to claim benefits, according to the life expectancy tables. So, if you claim at age 62 your monthly benefit will be considerably smaller than if you claim at age 66—but you’re likely to collect those benefits for a greater number of years. Conversely, a later claim will give you a higher monthly benefit—but for a shorter period of time.

But life expectancy is not the end of the story, because no one simply lives to the average lifespan. Some will beat those figures, and unfortunately, some of us will fall short of them.

The current Full Retirement Age (FRA) is 66 for most people getting ready to retire). If you claim before your FRA, your initial benefit will be reduced a certain amount for every month you claim early. If you file 60 months before FRA, for example, your benefit is reduced by 30 percent—permanently. And if you delay your claim beyond FRA, you receive a delayed retirement credit, for every month of delay, up to age 70. For example, waiting one extra year beyond FRA gets you 108 percent of what you’d get at your FRA—for life. Waiting a second year, until 68, gets you 116 percent.

Here’s a simple way of looking at this. A person with an FRA of 66 who claims at age 62, will receive a reduced benefit for the rest of his or her life—25 percent lower. Claiming at FRA is worth 33 percent more in monthly income than a claim at 62, and a claim at age 70 is worth 76 percent more.

Another key point: you don’t have to wait until 70 to benefit. Any delay is helpful for most people, and delay beyond FRA or just a couple of years can be very beneficial. If you do plan to delay, the key question is how to meet living expenses while you wait. If you’re still working, you’ve got that covered. If not, several strategies are available, depending on your situation.

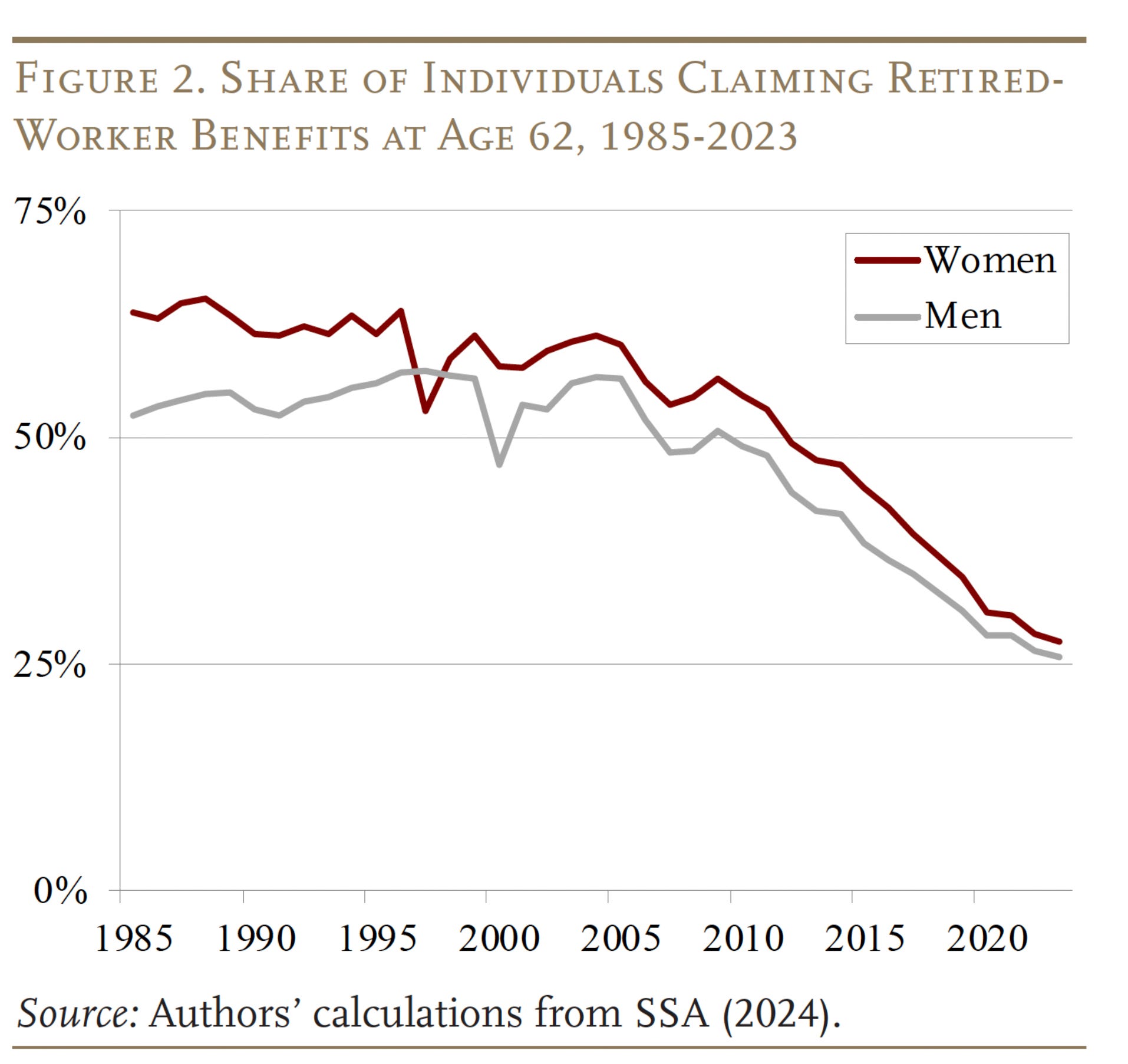

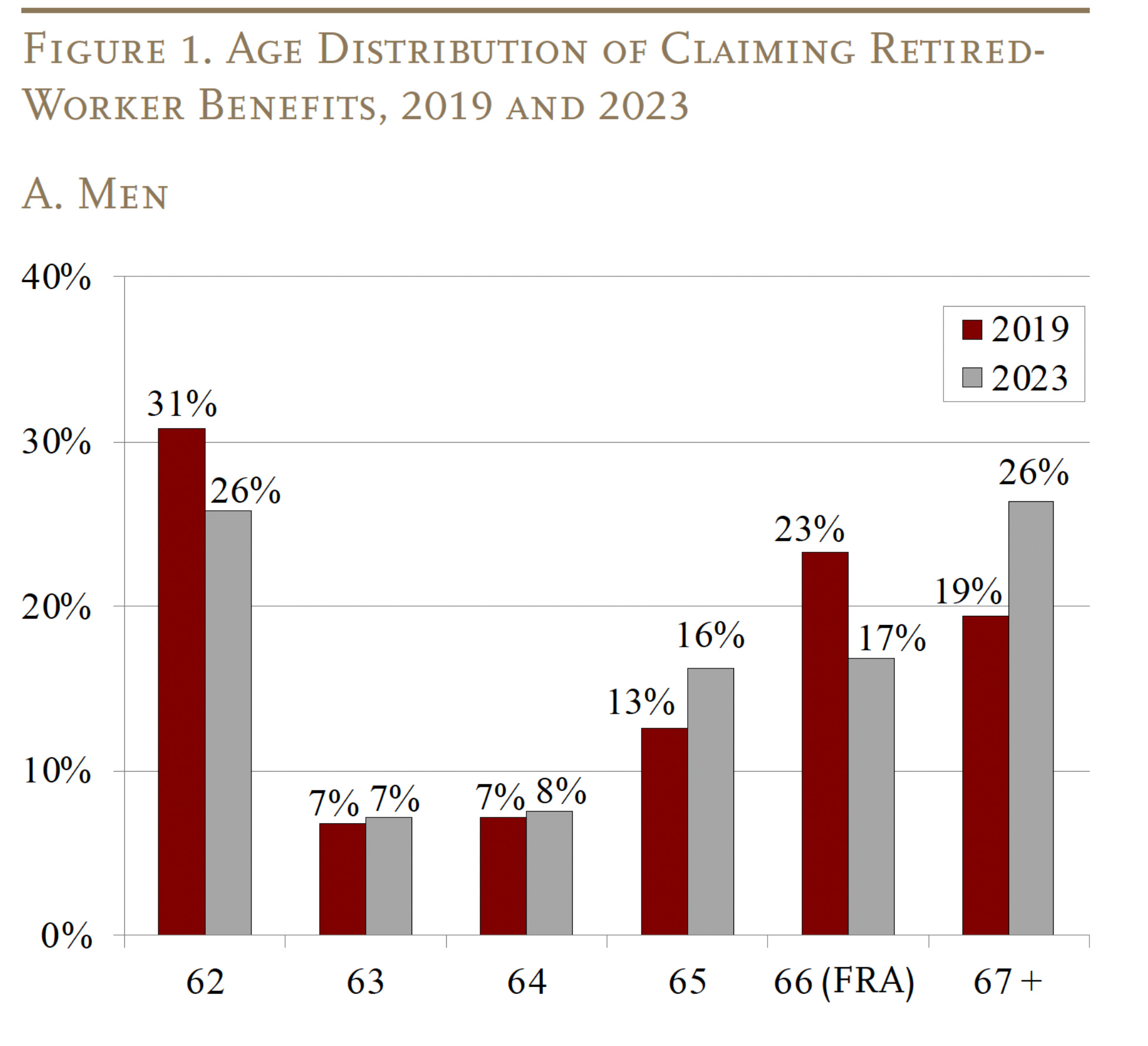

When do people actually claim?

For years now, retirement planners and the media have been talking up the advantages of delayed claiming -and the message has been getting through - the share of people claiming at age 62 has been falling. The Center for Retirement Research at Boston College has published an updated analysis of recent claiming trends. It shows that the share of Americans claiming at 62 has continued to decline, and the share that is waiting until age 67 or later is rising.

Here’s how the trends look for men and women:

Notably, COVID did not impact the trend. Many analysts expected the sudden loss of jobs that came with the lockdown would accelerate claiming, but it just didn’t happen.

Check out this sleight of hand on Social Security’s finances

The conflation of Social Security’s financial health with DOGE allegations of widespread waste, fraud and abuse in the program continues. New Social Security Administration commissioner Frank Bisignano gave an interview last weekend to Maria Bartiromo of Fox News, who lost no time describing him as the man “tasked with avoiding the expected insolvency of Social Security.”

That’s fundamentally false. The commissioner of the SSA is one of six trustees tasked with overseeing the Social Security trust funds, and the agency’s actuaries prepare the report. But it’s up to Congress to address Social Security’s finances. The report simply paints a picture of the program’s finances, and forecasts its outlook. Mr. Bisagnano’s job is to run the huge SSA bureaucracy, not to make policy.

But notice the Fox sleight of hand here - the network is conflating elimination of waste, fraud and abuse with the solvency of the trust fund. And that math just doesn’t add up - the amounts of improper spending don’t even come close to what’s going to be needed to avoid trust fund exhaustion in 2035. The government’s own research found that from 2015 to 2022, the SSA paid out almost $8.6 trillion in benefits and that less than 1% of that was in improper payments. Most of that due to record-keeping errors or delays, and ultimately corrected.

Bartiromo also spent considerable time during the interview interrogating Bisagnano about Elon Musk’s already-debunked charge that 150-year-olds are receiving Social Security. She seemed to acknowledge that this wasn’t happening, but then wondered if fraudsters might somehow be using Social Security numbers to enroll improperly in Medicare or Medicaid:

We don't know if they've actually accepted money, but we know that they could be using their number in different ways, like, for example, they could be using the number to get Medicare and Medicaid.

Medicare stopped using Social Security numbers as identifiers about five years ago, shifting to a system of unique Medicare identifiers. One of the reaasons? Fraud prevention. And Medicaid identifiers are issued by states, not the federal government.

You can watch the interview here.

Retirement Illustrated: A graphic approach to planning

Retirement educator Steve Vernon has launched a series of graphic online chapters that use illustrations to tell the stories of pre-retirees and retirees as they navigate the decisions they face. “Readers of Retirement Illustrated will imprint their understanding by reading stories with visuals and thinking about probing questions,” Steve says. “It reaches a broader audience that doesn’t normally read or respond to text-heavy content.”

The series expands on research Steve conducted at the Stanford Center on Longevity on retirement decision-making and behavioral economics. “It focuses just on the most important decisions and keeps it simple,” he says. “Too often, retirees think that retirement planning involves investing, and they overlook decisions that will have the greatest impact on their financial security and enjoyment of life.

What I’m reading

What Social Security could teach DOGE about efficiency . . .The perils of elderspeak . . . What UnitedHealth’s stock drop reveals about Medicare Advantage . . . A longevity expert’s five tips for aging well.