How Trump's federal workforce purge could impact Social Security customer service

Plus: Most Americans say they're OK paying more in taxes to keep Social Security solvent

People who need to do business with the Social Security Administration have been grappling with declining service for years - the result of budget cuts imposed by Congress at a time when an aging country’s demand for services are growing. The pandemic also rocked the SSA and made it much tougher for some people to apply for benefits.

Between 2010 and 2024, the SSA’s customer service budget fell 19% after inflation, and its staffing fell 11%. At the same time, the number of Social Security beneficiaries grew by over 13 million, or 25%. People trying to interact with the SSA have been reporting wait times on the toll-free number of an hour or more. The backlog of pending disability insurance applications is shocking - more than one million claims are pending. That’s not just an inconvenience, but a matter of life and death for some.

Another looming problem: implementing the recent repeal of the Windfall Elimination Provision and the Government Pension Offset likely will be very slow. The repeal legislation calls for the restored benefits to be paid starting with retroactive payments for 2024. Social Security officials have indicated that these benefit recalculations will be complicated and time-consuming. If you are among the affected retirees, I wouldn’t hold my breath waiting for a benefit adjustment.

Two Trump administration moves threaten to worsen the situation.

The blanket “deferred resignation” offer made to federal workers could further hollow out the SSA’s workforce, and I’m especially concerned that older, experienced people will decide to leave. Even if budget dollars become available to replace them (which is doubtful), training new SSA employees typically takes a year or more, since there are complex systems and rules to learn.

The White House “return to work” order also will shake the SSA. When the pandemic struck, the agency pulled off the difficult feat of shifting to a 100% virtual work environment during the lockdown; later, the unions representing the SSA workforce battled the agency over the question of return to the offices. That fight ended with a contract agreement spelling out a hybrid approach, which was extended in December through 2029.

The return to work order conflicts with that agreement. It will be litigated, but the uncertainty also could contribute to further brain drain.

Kathleen Romig of the Center for Budget & Policy Priorities summarized the situation well in this post on Bluesky:

This earlier post by CBPP’s Paul Van de Water offers further background on the SSA’s problems. Also see this earlier Government Executive story outlining the agency’s budget and service challenges.

Will DOGE tamper with Social Security and Medicare payments?

Alarms are going off in Washington, D.C. in the wake of the seizure of the Treasury Department's payment system by Elon Musk's Department of Government Efficiency (DOGE). It’s a completely unprecedented and troubling move.

Democrats and consumer advocates worry that DOGE’s access to the Bureau of Fiscal Service at Treasury gives them control over disbursement of trillions of dollars in payments each year - including Social Security benefits and Medicare payments. DOGE also gained access to sensitive data such as the Social Security numbers of most taxpayers.

Meanwhile, DOGE staffers also have been working at the Centers for Medicare and Medicaid Services, the Wall Street Journal reported yesterday, and they “have gotten access to key payment and contracting systems, according to people familiar with the matter.”

“The DOGE representatives have been on site at the agency’s offices this week, the people said, and they are looking at the systems’ technology as well as the spending that flows through them, with a focus on pinpointing what they consider fraud or waste. DOGE representatives are also examining the agency’s organizational design and how it is staffed, the people added.”

Is there fraud and abuse in the Medicare and Medicaid programs? Yes. The latest report of the Health and Human Services Inspector General found nearly $3 billion in improper payments. Not nothing - but for perspective, keep in mind that federal outlays last year for the two programs totaled approximately $1.5 trillion. In programs this large, there’s bound to be some fraud and abuse. (By the way, the HHS OIG, Christi Grimm, was among the OIGs fired by Trump last week).

If Musk really wants to uncover waste in the Medicare program, I direct his attention to the Medicare Advantage program. These plans were paid 22% more per capita than traditional Medicare, according to the Medicare Payment Advisory Commission (MedPAC), the Congressionally authorized watchdog. The overpayment problems stem from aggressive coding of conditions by insurance companies (“upcoding”), a quality bonus payment system that insurers use to game the system, and more.

Could the Treasury situation impact Social Security benefit payments? It seems far-fetched, although the current pace of developments and general state of chaos means it’s impossible to rule out anything. The Treasury said in a letter to Congress that DOGE has “read-only” access to the payment system, meaning it cannot make any changes. But Wired magazine’s reporting contradicts that letter:

“A 25-year-old DOGE operative named Marko Elez in fact has admin privileges on these critical systems, which directly control and pay out roughly 95% of payments made by the U.S. government, including Social Security checks, tax refunds and virtually all contract payments. earlier this week that one of Musk’s engineers.”

There are plenty of reasons to be very worried about what’s going on in Washington right now. But I don’t see a reason to panic about Social Security benefit payments. At least, not yet.

CBS News has a good story explaining what’s going on.

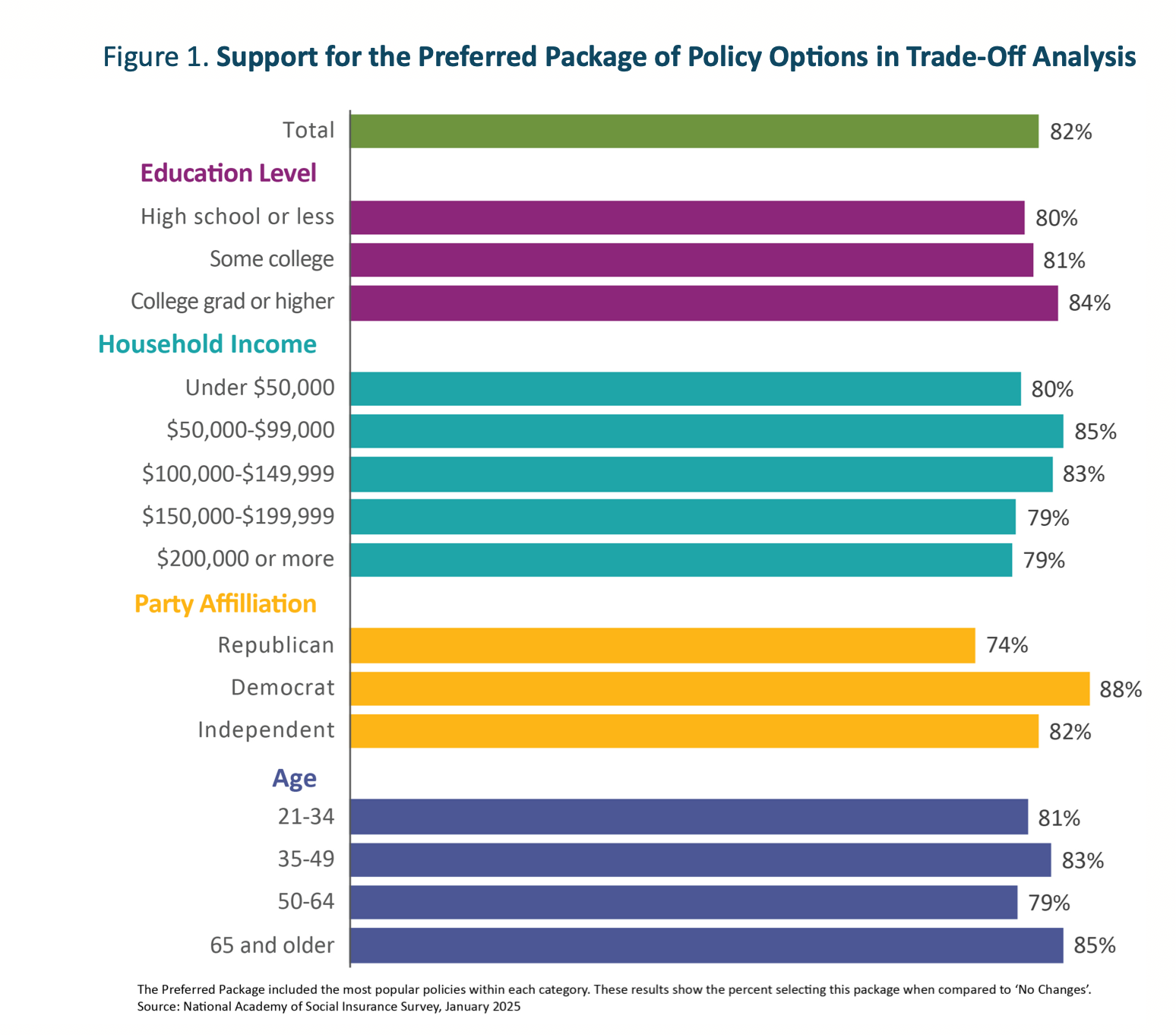

Most Americans would tax themselves to fix Social Security

Legislators often refer to “holding hands and jumping off the cliff together” when the subject is averting Social Security’s looming trust fund exhaustion. Absent action, benefits would need to be cut roughly 20% across the board in 2034. The “cliff jump” refers to the politically painful deal lawmakers think they think they need to make, which will be a combination of new taxes and benefit cuts. The argument: any solution must be bipartisan in order to win approval from Congress, so compromise is essential - in other words, spread the pain around and immunize one another from voter rage over benefit cuts.

But a different choice is available - don’t cut benefits. And that’s what most Americans would prefer.

That’s the key finding of a new survey that uses “trade-off analysis” to gauge public sentiment about solving Social Security’s financial problems. This approach is used in public opinion research to assess policy preferences by examining the trade-offs that respondents are willing to make among various options.

Here’s the key finding: the public shows a clear preference for revenue enhancements over benefit reductions. An impressive 85% of those surveyed advocate for maintaining current benefit levels, even if it necessitates tax increases for some or all Americans. The most favored approach involves eliminating the payroll tax cap for individuals earning above $400,000 annually. Additionally, there's broad support for gradually increasing the payroll tax rate to bolster the program's financial health, a sentiment that spans nearly all demographic and political lines. Conversely, proposals that involve reducing benefits are met with significant opposition. Options such as raising the retirement age further or adopting a slower cost-of-living adjustment formula are largely rejected by the public.

The study is being released during this 90th anniversary year of Social Security, and the sponsors include an interesting group of organizations representing a range of policy perspectives: the National Academy of Social Insurance and AARP (centrist), the National Institute on Retirement Security (progressive), and the U.S. Chamber of Commerce (conservative).

The details of the preferred package:

Beyond preserving existing benefits, Americans express a desire to see Social Security strengthened. There's notable support for targeted improvements, including introducing caregiver credits for individuals who take time off work to care for young children and establishing a "bridge benefit" to assist those in physically demanding jobs who may be unable to work until the full retirement age.

Rebecca Vallas, chief executive officer of the National Academy of Social Insurance noted: "At a time when our country is deeply divided, Social Security remains a powerful unifying force. This survey shows there is strong bipartisan agreement on how the American people want to secure the program’s future, and we urge policymakers to listen."

Don’t like your Advantage plan? The time to switch is now

I write every year about the importance of re-shopping Medicare coverage during the annual fall enrollment period, but there’s another enrollment period worth highlighting. That’s the Medicare Advantage open enrollment period that is underway now and ends March 31st.

If you’re not satisfied with your current Medicare Advantage plan, this is the time of year when you can switch to a different one - or to traditional Medicare. In either case, the opportunity is there only if you are currently enrolled in an Advantage plan.

And any move to traditional Medicare should be made with caution, as I told Yahoo! Finance columnist Kerry Hannon:

“Regular Medicare does not come with built-in caps on a variety of out-of-pocket costs, so you don't want to be enrolled in it without supplemental protection,” said Mark Miller, a retirement expert and author of “Retirement Reboot.”

For that you need a Medigap health insurance policy sold by private insurance companies that pays part or all of certain leftover costs. Medigap can cover outstanding deductibles, coinsurance, and co-payments and may also cover healthcare costs that Medicare does not cover at all like medical care received when traveling out of the US.

“In most states, the guaranteed right to buy a Medigap is limited to the time when you first sign up for Medicare Part B,” Miller said.

That’s because Medicare does not permit Medigap plans from rejecting you or charging a higher premium because of a pre-existing condition during that period. In most states, your premium, however, will vary depending on factors such as your age, gender, and where you live.

One of the most common complaints about Medicare Advantage plans is “prior authorization” - a technique widely used by insurance companies to ensure that health care services are medically necessary by requiring approval before a service or other benefit will be covered. Advantage plans use prior authorization to manage health care utilization and their costs (in other words, maintain profit levels). Typically, prior authorization is required for higher cost services, such as inpatient hospital stays, skilled nursing facility stays, and chemotherapy.

A new brief by KFF shows that use of prior authorization across the industry has been stable or down slightly, most likely in response to bad publicity and Biden administration efforts to regulate the practice more tightly.

This KFF chart shows which Advantage companies were more likely to request prior authorization for services in 2023.

I’ll have more to say about Medigap enrollment and plan selection in a story I’m working on right now. This piece will get under the hood on Medigap plan choices, and also compare the out-of-pocket exposure in traditional Medicare with the exposure you face in Medicare Advantage.

What I’m reading

Ozempic is among the next drugs set for Medicare negotiations . . . The centuries-long, very male quest to live forever . . . Sorry, but no secret to life will make you live to 110 . . . When the retirement community goes bankrupt . . . Even adults may soon be vulnerable to childhood diseases . . . A growing portion of murder-suicides, while rare, are affecting older adults. . . . Boomer women are shaping the largest wealth transfer in history . . . The health insurance system is a death sentence, some doctors say . . . The bond market is sending a warning about the economy . . . A useful summary of tax numbers that have (or haven’t) changed for 2025 . . . How climate change will impact home values in the years ahead . . . CEO explains Vanguard’s biggest fee cut ever . . . The scientific fight over whether aging is a disease.