Is Medicare Advantage really cheaper?

More than half of Medicare enrollees have chosen Medicare Advantage plans - the all-in-one commercial alternative to the traditional program. The rapid growth of Advantage in recent years has been fueled by extensive marketing emphasizing lower premiums, extra benefits, and claims about protection against high out-of-pocket costs.

Advantage plans can indeed save you money upfront. Many include prescription drug coverage and charge no additional plan premium beyond the Part B premium. You don’t need a supplemental Medigap plan to cap out-of-pocket (OOP) costs, because Advantage plans come with their own built-in caps.

But the comparisons sidestep a critical question: what’s your financial exposure in a Medicare Advantage plan if you get sick and need a great deal of care?

A new brief by KFF, the health care research group, takes a deep dive into this question.

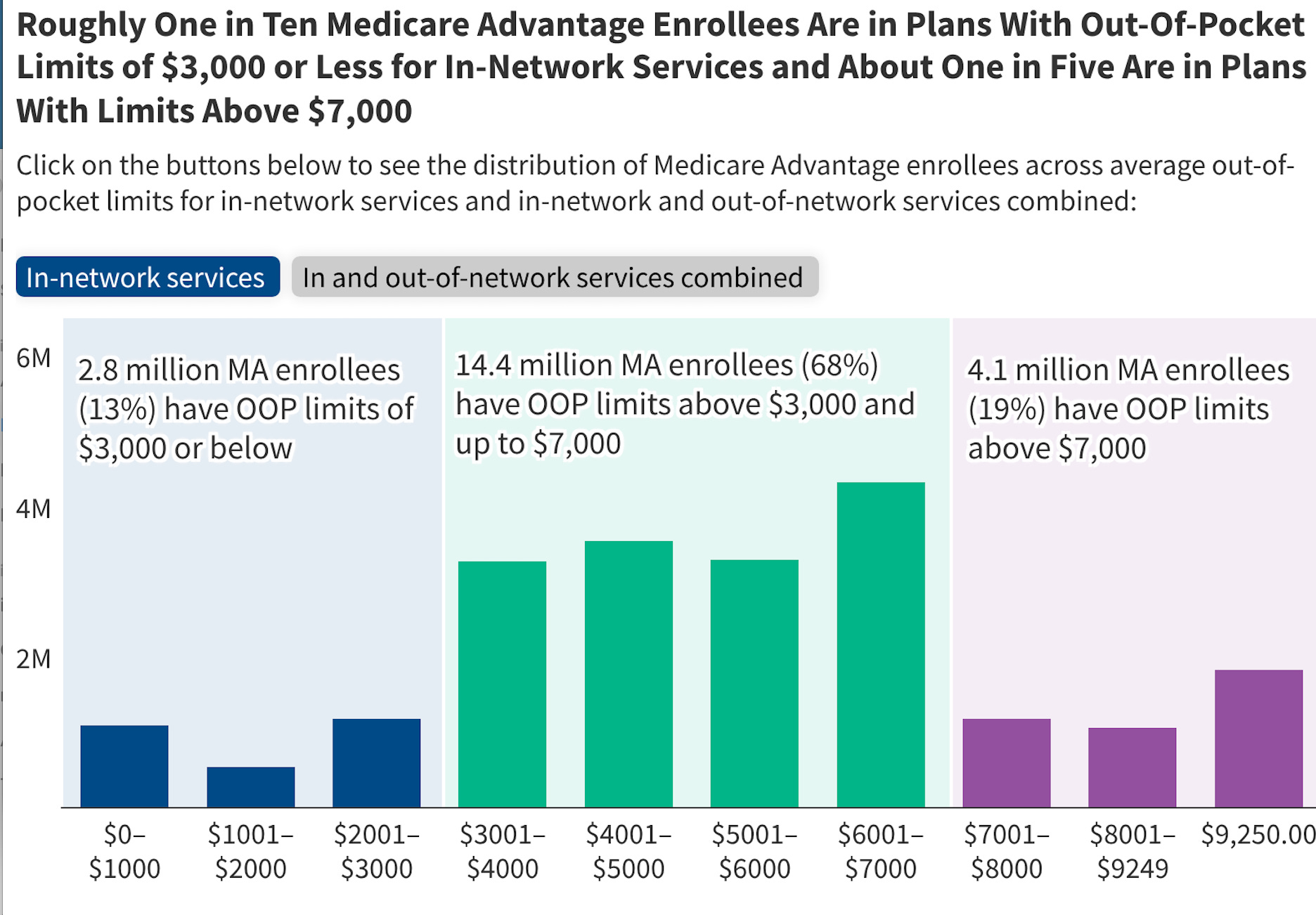

The federal government sets maximum OOP amounts for Advantage plans. This year, the in-network ceiling is $9,250, but many plans set lower limits to win marketshare. This year, the average Advantage plan capped in-network OOP outlays at $5,421, and $9,825 for in-network and out-of-network combined, according to KFF.

At first glance, that in-network cap seems reasonable - assuming that you’re willing to stay in-network - considering that a Medigap plan might set you back $2,000 or more in some parts of the country.

Most Medicare Advantage plans are either HMOs, which generally require beneficiaries to use network providers except for emergencies and certain limited situations, or PPOs, which allow out-of-network care at higher cost.

The KFF analysis measures the financial exposure beneficiaries face in their plans - it doesn’t indicate how many enrollees actually reach these spending limits in a given year, because that data isn’t available. But the brief does look beyond the average OOP caps - and the figures here are revealing. Many beneficiaries are protected by relatively modest caps, but millions are exposed to high OOPs before reaching their plans' limits:

About one in 10 Advantage enrollees are in plans with the maximum out-of-pocket limit for in-network services ($9,250). Among the 8.6 million enrollees in PPOs, roughly one in five (22%; 1.8 million) are in plans with the maximum out-of-pocket limit for in-and out-of-network services combined ($13,900).

At the other end of the spectrum, 13% of all Advantage enrollees are in plans with out-of-pocket limits of $3,000 or less for in-network services. But nearly all of them are in HMOs, which have the tightest restrictions on the health care providers you can see.

This KFF chart depicts the spread just for in-network services (to see the in and out-of-network combined cap, visit the brief online and click the button for that data, currently shown against a gray background).

The numbers show that it’s critically important to consider your overall protection against high OOP costs when selecting an Advantage plan. Review your coverage during the annual enrollment period that runs from October 15 - December 7th. Also pay careful attention to the list of in-network providers and confirm with your health care providers that they will be in the plan you’ve selected for the coming year. And, make sure your prescription drugs will be covered.

You also can leave Advantage and shift to traditional Medicare during the annual fall enrollment period - with one caveat. Before making the switch, verify that you can obtain Medigap coverage at a price you can afford. In most states, insurers may deny coverage or charge higher premiums based on health status once your initial Medigap enrollment window has closed.

When you first sign up for Part B, Medigap plans are required to accept you — and can’t charge more — regardless of pre-existing conditions. This “guaranteed issue” right applies during your six-month Medigap Open Enrollment Period, which begins the first day of the month you turn 65 (or older) and are enrolled in Part B.

After that window closes, most states allow Medigap plans to reject applicants or charge higher premiums based on pre-existing conditions. Four states offer broader protections: Connecticut, Maine, Massachusetts, and New York.

Other KFF research has found that traditional Medicare paired with a Medigap may provide more predictable long-term costs. While Medigap coverage requires an additional premium, it can substantially reduce or eliminate out-of-pocket costs, depending on the plan you select.

Learn more about how to shop Medigap here.

If you want to switch this fall, start by shopping the Medigap market using the federal Medicare plan finder tool and then apply for a plan that looks good to you. The insurance company will walk you through a “medical underwriting” screening by phone before approving your application. If you’re accepted, you can then disenroll from Advantage. Traditional Medicare will now become your default enrollment.

The true test of any health plan isn't what it costs when you're healthy—it's what it costs when you're not.