New Alzheimer’s drug holds promise but adds cost pressures for Medicare

Federal officials gave the green light last week to an expensive new drug that may be able to slow the advance of Alzheimer’s disease - a decision that might sound like a repeat of a story you’ve already read about soaring Medicare premiums and controversy over drug effectiveness.

But the story of Leqembi likely will be different than the drama surrounding another drug for treating Alzheimer’s that rolled out in 2021.

That year, the U.S. Food and Drug Administration approved a drug called Aduhelm despite objections from the agency’s own scientific advisory panel. Doubts about the drug’s safety and effectiveness ultimately led Medicare officials to sharply limit its use - but not before the program increased the Part B premium for 2022 by a whopping 14.5% to fund expected Aduhelm expenses. Medicare later adjusted course by making an unusual downward adjustment in the 2023 premium.

Leqembi was developed by Japanese pharmaceutical company Eisai, and it is marketed in the U.S. through a partnership with Biogen, the maker of Aduhelm. In clinical trials, Leqembi has shown more promising results than Aduhelm - it may slow patient decline by about five months over an 18-month period for people with mild Alzheimer’s symptoms. Some Alzheimer’s experts are not convinced that the benefits will be meaningful, and there also are concerns about side effects that include brain swelling and bleeding.

Medicare announced that it will cover Leqembi for patients with mild cognitive impairment or mild dementia, although it also will require physicians to participate in a data-collection effort to monitor the drug's effectiveness and risks.

But the approval of Leqembi also will put new upward pressure on Medicare premiums, and it casts a fresh spotlight on escalating drug costs borne by the Part B program. Drugs like this are administered in clinical settings - Leqembi comes as a twice-monthly infusion. In Part B, enrollees are responsible for 20% copays on all health services. If you’re enrolled in traditional Medicare with a Medigap, some or all of that cost would be covered. But everyone else - including people in Medicare Advantage plans - will be paying a hefty annual price tag of around $5,000.

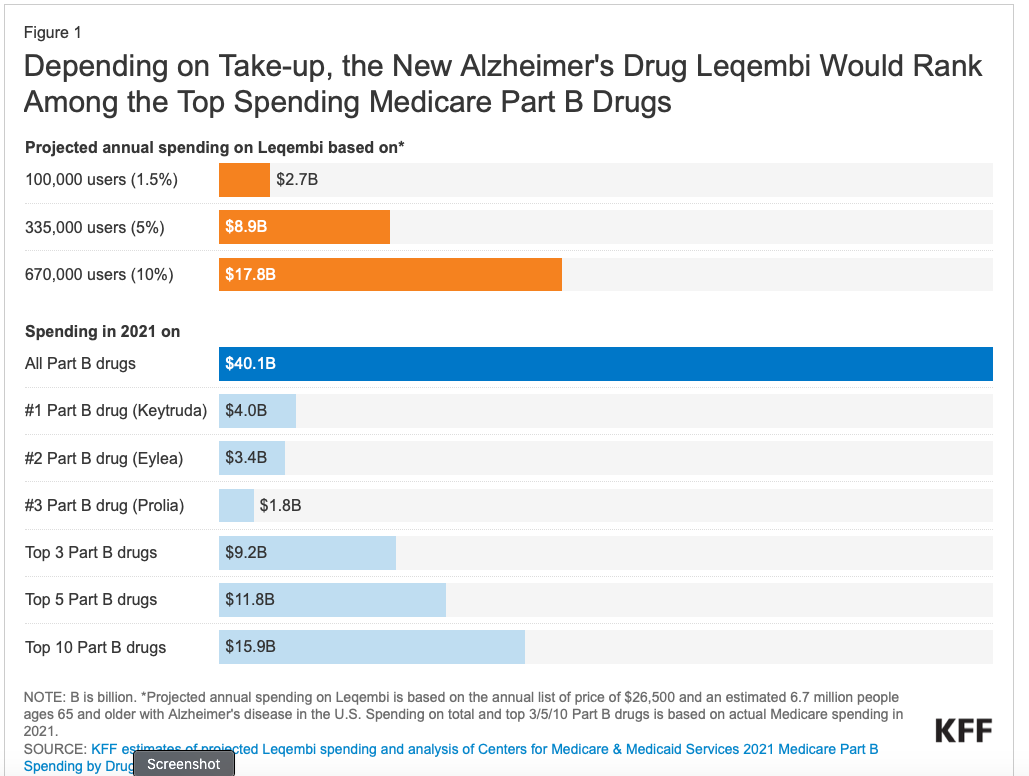

The Medicare program’s share of the cost will be covered by general government revenue and all Part B enrollees through the premiums they pay. That raises the question of whether Leqembi will lead to a repeat of the Aduhelm Medicare premium mess. The Kaiser Family Foundation notes that the answer depends on how many Alzheimer’s patients take the drug - and the speed of uptake. The drug’s manufacturers have estimated that about 100,000 patients will use it over the first three years of availability. If that estimate holds, KFF estimates that annual Part B spending on Leqembi would be $2.7 billion, making it the third-most costly drug covered by Part B. If take-up rates are higher, impact on Part B premiums could be much higher.

Learn more in my latest Reuters column. And Howard Gleckman offers a good Q&A on the new drug at Forbes.

Social Security COLA for 2024 likely will be around 3%

With inflation cooling off, next year’s Social Security COLA is tracking toward a 3% bump. That forecast is based on the latest Consumer Price Index released this week. As per above, Leqembi could have an impact on the net Social Security COLA if it leads to a substantial bump in Part B premiums. (Premiums typically are deducted from Social Security checks.).

I’ll be writing more about the COLA this fall as the data continues to firm up.

In case you missed it: states tackle long-term care insurance

A handful of states are taking action to help protect residents against the risk of high long-term care expenses. This month, Washington State will start the WA Cares Fund, a public long-term care insurance program. California is considering a similar plan. Minnesota and several other states are studying options. Learn more in my latest column for The New York Times.

Listen: Bill Bernstein on the four pillars of investing

When Bill Bernstein talks, people listen (to borrow an old Wall Street ad slogan). Bernstein is a neurologist turned investment advisor, and the author several books, including The Intelligent Asset Allocator, The Four Pillars of Investing, If You Can: How Millennials Can Get Rich Slowly, and The Delusion of Crowds. Bill has just issued a new edition of The Four Pillars of Investing, and he recently appeared on Morningstar’s podcast, The Long View, to offer his current take on financial markets.

Hosts Christine Benz and Jeff Ptak quizzed Bernstein on a range of important topics for retirement investors:

How retirees should think about asset allocation

The outlook for market returns

Bond ladders constructed using Treasury Inflation Protected Securities (TIPS)

Why Bernstein is not a fan of annuities.

So, here we have two smart interviewers talking with one of the smartest people you can find on the topic of financial markets. It’s worth a listen!

You can find The Long View wherever you get your podcast, or here.

What I’m reading

Rising temperatures threaten more than misery for oldest Americans . . . Corporate pension buyouts doubled in the first quarter . . . Study raises concerns about access to psychiatric services in Medicare Advantage plans . . . Three vaccines envisioned to avoid “tripledemic” this winter . . . Substance abuse rises among older adults . . . How to leave grandkids your retirement savings, but not a huge tax bill . . . Private equity firms tighten their grip on speciality medical practices . . . The longevity clinic will see you now -for $100,000 . . . Why credit scores still matter in retirement . . . Should state long-term care insurance funds invest in stocks?