When the stock market goes through a stomach-churning drop, retirement investors are naturally inclined to want to do something about it.

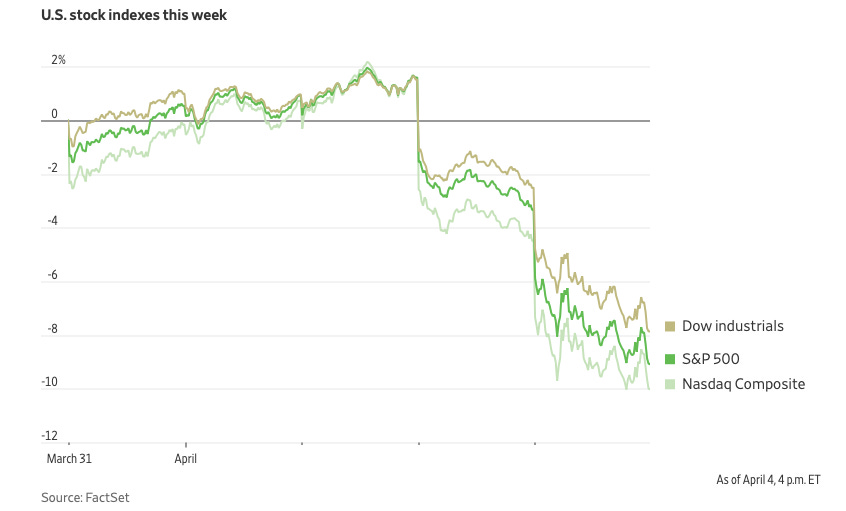

We certainly are at such a point now. The Dow Jones Industrial Average finished on Friday down 14.9% from its recent high. The Nasdaq Composite is down 22.7% from its recent high. (When markets drop more than 20%, that’s consider a bear market.).

But doing “something” just might be your worst move.

The time to act is before the market gets rough. I don’t know where the market is headed this week, this month or this year - and neither do you. Will Trump’s tariffs stick or not? How significant an economic impact will they have? Are we headed for a recession? How will the Fed react?

We can’t predict the future, but there are three core principles of investing for retirement that can really help you sleep at night at moments like this:

Diversification: invest in low-cost mutual funds that invest in thousands of companies - far more than you could ever select, track and manage on your own. That gives you a measure of safety, since your exposure to sharp movements in any one stock or market sector is reduced.

Balance: Invest in more than one type of asset (typically equities, bonds, and cash securities). This spreading out of investments is helpful because in any given year, one of these asset classes might be up while another is down. Balance helps smooth out the ups and downs. This can be done within a specific fund, or by owning two or three different types of fund that give you a reasonable balance among different investment types.

Allocation: Make a thoughtful decision about your exposure to equities that reflects both your tolerance for risk and the goals you are trying to achieve. The challenge at times like this is sticking with that allocation mix as market shifts distort your percentages. This is achieved through periodic rebalancing of the portfolio - when stocks are riding high, you sell enough to bring your allocation back to the targeted level and reinvest the proceeds in an asset class that is down. Rebalancing is a sell-high, buy-low discipline that can boost your portfolio performance significantly over time. It’s not something you need to do frequently - perhaps two or three times each year. If you are invested in a target date fund (more on that below), your funds will be rebalanced automatically by your fund management company.

Jack Bogle, the founder of Vanguard and the pioneer of low-cost passive mutual funds, often pointed out the fallacy of stock picking. Here’s what he said in an interview with AARP before he died in 2019:

Absolutely no one knows what the stock market is going to do tomorrow, let alone next year. Nor which sector, style or region will lead and which will lag. Given this absolute uncertainty, the most logical strategy is to invest as broadly as possible and benefit from the compounding of dividend yields and long- term earnings growth of American—and global—corporations.

Perhaps Bogle’s biggest achievement was getting everyday investors to understand the importance of minimizing fees charged on portfolios. He taught that it’s not just a matter of what you invest in and how your selections perform—it’s also about how much ends up in your pocket after the fund management company takes its cut. This is a key ingredient of the Bogle-led revolution that has spread far and wide in the mutual fund industry—the simple notion that investor outcomes are dramatically better when costs are lower.

It’s difficult to overstate the importance of this tenet, and the magnitude of the change that has occurred in the industry. The year of Bogle’s death, the Vanguard Group was putting about $21.1 billion annually into the pockets of investor accounts that otherwise would have gone to fund companies as fee income. And that doesn’t begin to measure the knock-on effect of lower fees charged by all of Vanguard’s competitors, who have been forced to reduce fees in order to stay in business.

If your investment strategy isn’t aligned with the principles I’m outlining above, give some thought to getting there. I’m not suggesting any rash, quick moves - especially considering the current volatility. As Morningstar’s Christine Benz notes - first, do no harm:

Dramatic market losses can spark real emotions (anxiety, powerlessness), and it can be tempting to take dramatic portfolio measures in response. With cash yields decent relative to recent history, the stability of money market funds or CDs might look like a tempting and reasonably profitable way to escape the cacophony of the market. You do need some liquid reserves in your portfolio (more on this in a minute), but resist the urge to shift out of stocks entirely. Such a move could buy you some short-term relief, but it will soon be replaced by another nagging worry: Is it time to get back in?

Markets like the one we’re experiencing now are toughest for do-it-yourselfers accustomed to placing big bets on individual companies or sectors. Over the past few decades, the evidence clearly shows that adhering to these three principals - not stock-picking - yields the best long-term results.

Moreover, retreating to cash only protects you from one risk—further equity losses—but it doesn’t safeguard you against other key trouble spots—specifically, inflation risk or the chance that you’ll outlive your money because your portfolio didn’t grow as much as it needed to. A better plan is to maintain a stock/bond mix that makes sense relative to your goals, life stage, and proximity to needing your money, then rebalance back to your targets periodically. A balanced asset allocation will make sense for most people approaching or in retirement, whereas a more equity-heavy mix will suit investors under 50.

But the current market quakes do offer an opportunity to make a thoughtful plan for change.

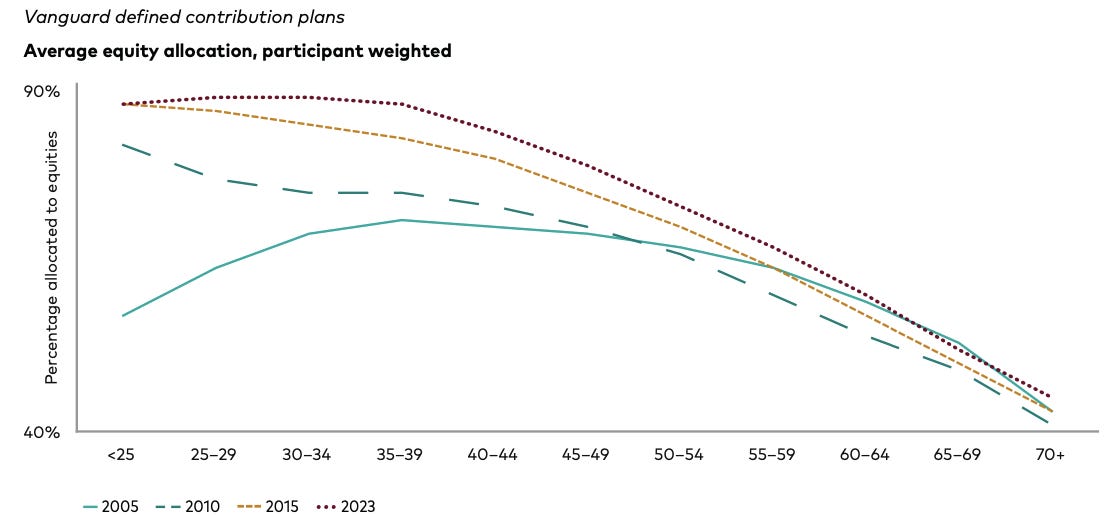

The end of hump-shaped equity allocations

The chart above depicts the change in equity allocation in 401(k) plans managed by Vanguard by age group over the past two decades. It’s a good news story about the rise of automatically-managed investment portfolios.

In 2005, age-based equity allocation was “hump-shaped,” notes Vanguard. Younger participants had conservative allocations, middle-aged participants had the highest equity exposure, and older participants had equity exposure similar to younger participants. In 2023, the equity allocation of Vanguard DC participants was downward sloping by age.

That’s mainly due to the rising dominance of target date funds, which automatically adjust and rebalance your portfolio as you get closer to retirement. A smaller trend is the rise of managed account advice within plans.

The biggest change is among younger investors. People in their early 30s went from an average 69% equity allocation in 2005 to 89% in 2023. That’s appropriate, since young retirement investors have many decades ahead of them to ride out market downturns.

The allocations among older investors nearing retirement didn’t change nearly as much. People age 60-64 are about 60% invested in equities, about as they were in 2005. For the 65-69 year olds, the allocation in 2023 was 52% - about the same as in 2005.

Some critics argue that these allocations are too risky - precisely because of market conditions like we’re experiencing now. Savers who need to tap their savings right now do so at a loss. The approach to equity allocations varies quite a bit among the fund management companies. Some argue that the higher stock allocations are necessary to prolong portfolio life in retirement. Others take a more conservative approach.

But TDFs have helped millions of retirement savers stay on track with a more appropriate asset allocation. And automating your portfolio has one other big advantage: it can help you avoid becoming your own worst enemy by paying too much attention to your portfolio and making all-too- human moves, like market timing, panic selling, and euphoric buying.

As Bogle said in that AARP interview, “You’ve heard the phrase ‘Don’t just stand there, do something’? For investors, by far the better advice is ‘Don’t do something, just stand there.’”

What I’m reading

Dr. Oz was confirmed to lead the agency that runs Medicare . . . The longevity business is booming, but its scientists are clashing . . . Roth IRAs are all the rage among young savers . . .Obamacare enrollees could see big changes in 2026 . . . Cracks appear in Congressional support for Medicare Advantage . . .