Healthcare costs are rising at several times the rate of general inflation, and it’s one of the major financial challenges that retirees face as they struggle to maintain their standard of living. Nowhere is this more clear than in the annual interplay between the Social Security cost-of-living adjustment (COLA) and Medicare Part B premiums.

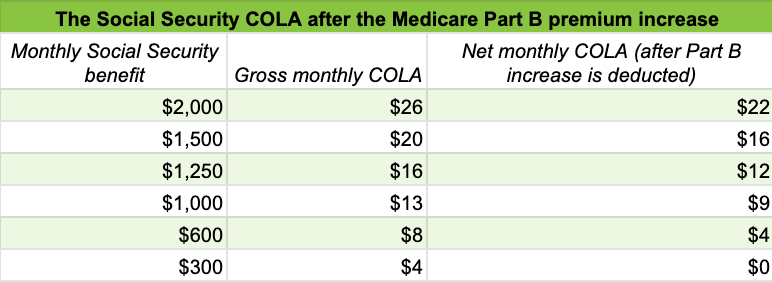

Last month, Social Security announced a 1.3% COLA for 2021. That’s a very meager increase, but it looks worse following Medicare’s announcement last week that the monthly standard Part B premium will rise $3.90, to $148.50. If you’re enrolled in both Social Security and Medicare, the Part B premium is deducted from your benefit, so its interplay with the COLA is important.

The impact varies depending on your Social Security benefit amount, as the chart below shows. For people with very low benefits, Medicare eats up most or all of the COLA; in cases where the Part B hike would be larger than the COLA, the Social Security benefit is unchanged due to the “hold harmless” provision in federal law, which prohibits any decrease in benefits.

This year’s Part B premium was on track to rise much more than $3.90 per month, but a COVID relief measure passed by Congress recently capped the increase at 25% of whatever it would have been if Medicare simply followed the usual formula.

Joining me on the podcast this week to walk through the changes for 2021 is Mary Johnson. Mary is the Social Security and Medicare policy analyst for The Senior Citizens League; she’s been tracking the COLA for more than 25 years, and knows this topic inside and out.

Mary points out that we’re really in an unprecedented situation with regard to COLAs. Over the past decade, we’ve had zero COLAs three times, and one year where the increase was just three-tenths of a percentage points. Over a 12-year period, the COLA has averaged just 1.4%. “Twelve years is about one-third of the length of time a person spend in retirement,” she says, “So that is having a significant impact on the lifetime retirement benefits you receive from Social Security.”

Listen to the podcast by clicking the player icon above. The podcast also can be found on Apple Podcasts, Spotify and Stitcher.

Not a subscriber yet? Take advantage of a special offer

Sign up now for the free or subscriber edition of the newsletter, and I’ll email a copy of my latest retirement guide to you. This one looks at how to think about timing your retirement in the age of pandemic.

Just a reminder- subscribers receive the full edition of the newsletter (the free edition is abridged), and they have access to the entire series of guides at any time. Click on the little green button to subscribe, or go here to learn more.

Medicare marketplaces really don’t work very well

Every fall, you get the barrage of messages. It starts with the Annual Notice of Change document that Medicare sends, listing the changes in your current Part D or Advantage plan coverage. Then there’s the “Medicare & You” handbook containing detailed information about plan options. A flurry of email alerts urging you to shop your coverage using the Medicare Plan Finder website also go out each fall.

Insurance companies flood the airwaves and mailboxes with advertisements and brochures. Journalists like me nag you about this with our columns and newsletters!

None of it is working very well. A new study by the Kaiser Family Foundation finds that 57 percent of Medicare enrollees don’t review or compare their coverage options annually, including 46 percent who “never” or “rarely” revisited their plans. Strikingly, two-thirds of beneficiaries 85 or older don’t review their coverage annually, and up to 33 percent of this age group say they never do. People in poor health, or with low income or education levels, are also much less likely to shop.

Why? Tricia Neuman, a co-author of the Kaiser report, sums it up:

“A large share of the Medicare population finds this whole task pretty unappealing, and they just don’t do it. That raises questions about how well the system is working.”

If you’re enrolled only in Original Medicare with a Medigap supplemental plan, and don’t use a drug plan, there’s no need to re-evaluate your coverage. But Part D drug plans should be reviewed annually. The same applies to Advantage plans, which often wrap in prescription coverage and can make changes to their rosters of in-network health care providers. Plans can change the monthly premium as well as the list of covered drugs - and they can change the rules around your access to drugs, or impose quantity limits or require prior authorizations.

The findings call into question just how well privatization of Medicare is working - if you don’t have willing, tuned-in buyers, how well can a marketplace really work?

I explore that question in my latest Retiring column for The New York Times, which was published today.

Along with the column, here are a few more thoughts on this topic:

Medicare has not always been this way: At its creation in 1965, Medicare was envisioned as a pure social insurance program, with everyone paying in the same amounts and receiving the same coverage. But with the expansion of drug coverage in 2003 and the rapid growth of Medicare Advantage, we’re headed toward a system of marketplaces with the original program increasingly looking like a public option. Advantage is projected to account for 64% of enrollment by 2028, according to Avalere Health:

A different approach is possible: A standard benefit in Medicare, funded through premiums and payroll taxes, would work just fine - especially if we change the law to permit the federal government to negotiate drug prices, just as the VA and Medicaid can do. That’s prohibited under the law that created Part D. What sense does that make?

Human behaviorand choice: The Medicare marketplace is a key example of the choice-driven ideology that has driven so much of our retirement system over the past four decades. We have shifted decision making and risk from the sponsors of benefit plans to participants - the poster child being the move from defined benefit pensions to defined contribution 401(k) plans. We know how well that is working - 401(k) account balances are concentrated among the wealthiest households, participation is flat and the decline of DB pensions has taken a huge bite from overall retirement security (see my write-up of the latest Federal Reserve data on retirement saving accounts in this recent newsletter edition).

All of these systems are wrapped up in ideology about competition and consumer choice. When will we wise up? It’s been proven over and over again that the best way to deliver retirement security to the majority of households is through our social insurance programs, so let’s beef them up, make them less complicated and as universal as possible.

Still time to shop this year

Here’s my last reminder of the year to revisit your Part D or Advantage coverage this fall. There’s still time - enrollment runs until December 7th.

Get assistance from your local State Health Insurance Assistance Program, the federally funded counseling service that provides free one-on-one assistance in every state; (use this link to find yours.)

The Medicare Rights Center offers a free consumer help line: (800-333-4114.)

You can browse plans on the Medicare Plan Finder, the official government website that posts stand-alone prescription drug and Medicare Advantage plan offerings. The plan finder now allows users to sort plans not only by premiums but for total costs, including premiums, deductibles, co-pays and coinsurance payments.

When it comes time to enroll, call Medicare to sign up at 800-MEDICARE (800-633-4227) and to ensure that your enrollment has been processed.

Social Security and retirement timing in the age of COVID: My discussion with Jean Chatzky on Facebook Live

Personal finance guru Jean Chatzky invited me to join her this week on Facebook Live to talk about Social Security, retirement timing and the pandemic. Jean conducts a great interview, and we spoke at length about how COVID-19 has impacted retirement planning, and altered Social Security claiming - you can listen to a replay here.

Join me for a panel discussion on the future of retirement

I’ll be joining a panel discussion next week on the pandemic’s impact on the outlook for retirement within workplace plans a bit later this month, moderated by my Reuters colleague Lauren Young. Also on the panel are Christine Benz of Morningstar, economist Teresa Ghilarducci, Kedra Newsom Reeves of Boston Consulting and Harry Dalessio from Prudential Retirement.

The session will be convened on Monday November 16th at 1pm eastern time. Registration is free, and the conversation will be provocative, so please join us (register here).